CIMB Research released a report today on oil & gas segment. Funny that their recommendation was ADD with a target price of RM0.89 which is a whopping 78% gain from this price.

Their argument was demand for jack up rigs to improve in 2018 and 2019 but data turn out otherwise.

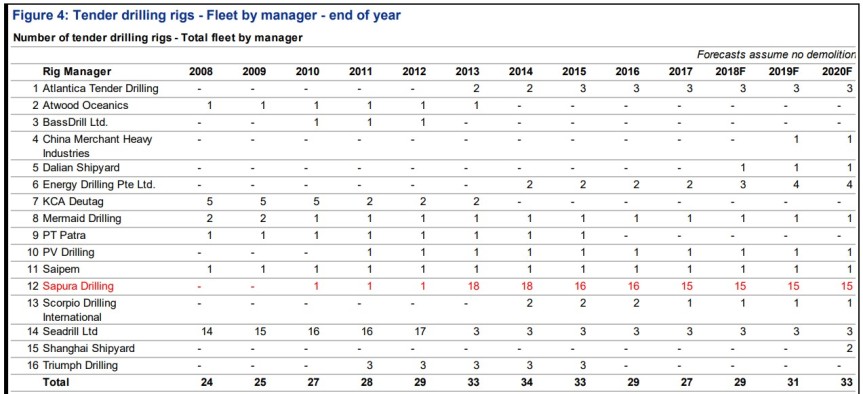

Rig Count

First up! Data on total fleet. The forecast came in as no growth for the next 3 years. This meant that the CAPEX isn’t going to happen, most of the cash could be used to pare loans. A good sign in general…

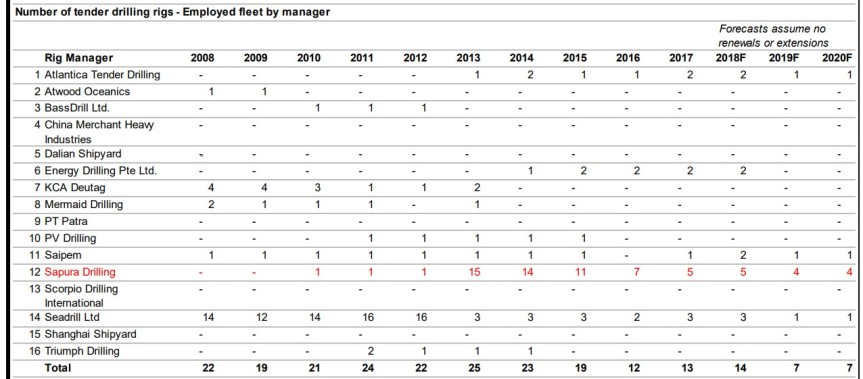

Utilisation

Second, the data below shows employed fleet and this number gets a little ugly. Out of the 15 fleet unit only one third of the drillers gets used over the next 3 years.

Indeed, you can argue that they could be signing new contracts in the future but the prospect ahead looks ugly for growth. Oil prices assumed to be floating near $75 – $80 which is still heavy on cost for sea drilling. The analyst places growth ahead being slow which is viable to the current industry condition.

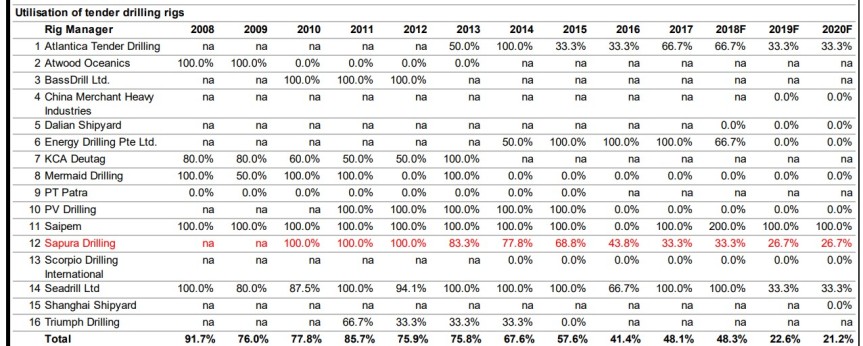

Another way to represent the data would be utilisation. If you look at previous years when Sapura used to be the jewel in the industry it had dropped significantly even when oil was super high in 2013 an 2014. The contracts weren’t renewing itself which causes the pain at the current moment.

Something definitely went wrong there and the suffering due to lower oil prices immediately gets translated into no contract renewals for 2014 – 2016.

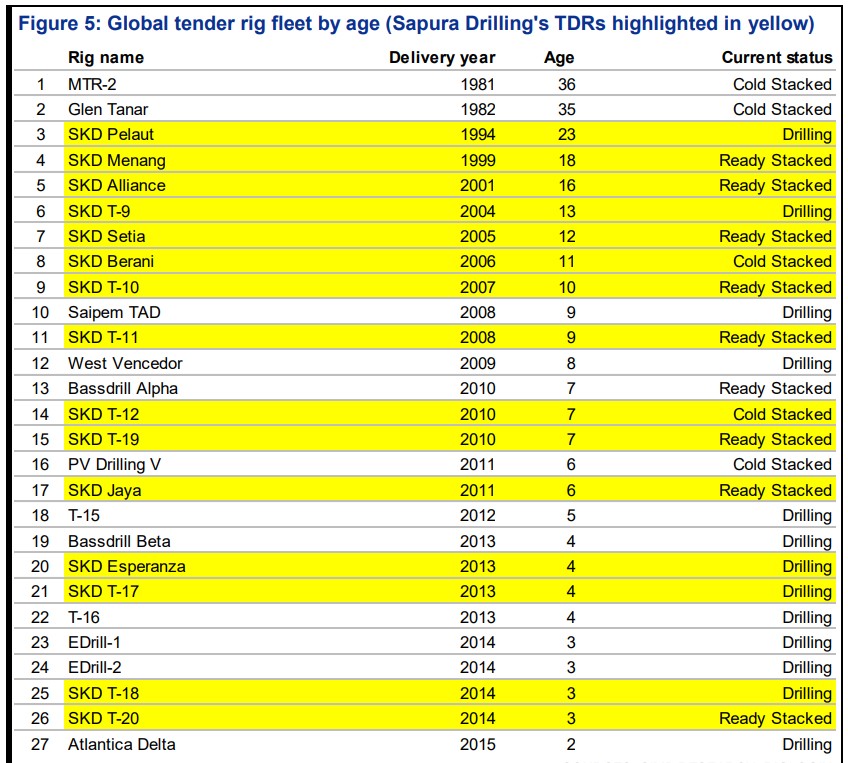

Rig Age

The next set of data shows rigs getting old as well. Another problem to take into account. We admit that we don’t have the info for how long these rigs are going to last but in the report by CIMB, it stated that the last three scrap was 35 years (2 units) and 28 years.

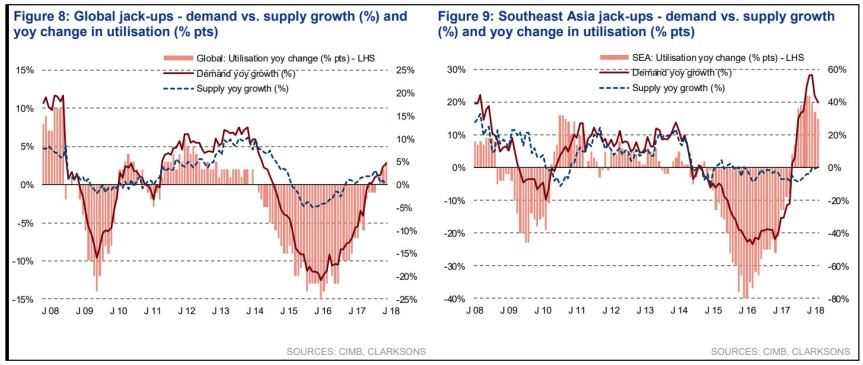

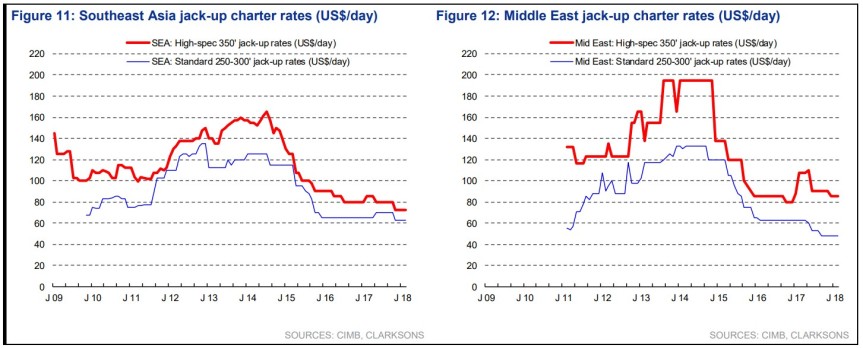

Industry Demand

Finally, demand came back with supply rates for jack-ups being low. Problem is the charter rates per day isn’t rising with the demand.

It is hard to digest how Sapura would be able to rise 78% to CIMB’s target price. The forward forecast for the next 3 years points to lower utilisation. It could only mean lower revenue and an even lower profit margin that could be derived due to higher interest rates and intense competition.

Stay Safe! – Credits to CIMB for all the data